(12 December 2023, Hong Kong) Hong Kong’s commercial property leasing and investment markets experienced a slower-than-expected improvement in 2023. As high interest rates and global economic slowdown persist, the road to recovery will remain bumpy and challenging in 2024, according to JLL’s Year-End Property Market Review and Forecast released today.

Joseph Tsang, Chairman of JLL in Hong Kong, suggested that the government implemented seven measures to provide crucial support for the housing and land markets in order to prevent a detrimental impact on the economy.

Key points:

- The total surrendered office spaces in the five major office markets dropped 27.2% y-o-yin 2023.

- Overall Grade A office rents will drop 5 to 10% in 2024.

- Some international retail brands are considering expanding their presence in the city.

- Rents of High Street Shops will rise 5 to 10% next year while rents of prime shopping malls will climb 0 to 5% only.

- Investment volumes involved corporate/occupier buyers increased by 1.05 times in the second half of 2023, compared to the first half of the year.

- Retail properties will outperform the overall investment market and their capital values will rise 0 to 5% in 2024.

- Mass residential prices will drop about 10% in 2024

- The government should take action to support the housing market and prevent negative impacts on the economy from the price correction.

- As of November, only 14.2% of the current fiscal year land premium revenue target was achieved.

- Resume government land sales by application list to increase the likelihood of successful land sales and avoid damaging knock-on effects on the market.

Office Market

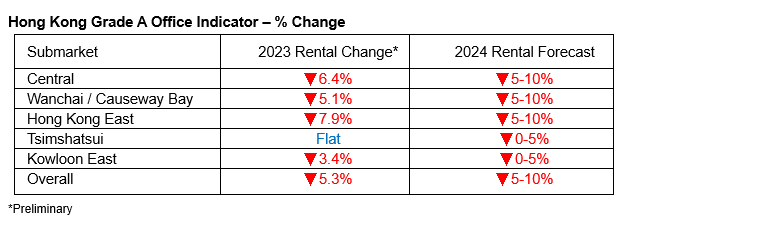

Office leasing market showed a moderate improvement in 2023, but at a slower than expected pace. The overall market experienced a positive net take-up in the second half of the year after the market recorded negative take-up in the first half. However, demand for Grade A offices remained subdued, leading to a 5.3% decrease in overall rents by the end of November. Tsimshatsui is the only submarket which saw rents staying firm due to limited availability of premium office spaces.

The vacancy rate of Grade A offices rose to 12.9% by the end of 2023, while Central’s vacancy rate increased to 9.9%. However, the total surrendered space contracted during recent years. The total surrendered office space in the five major office submarkets dropped 27.2% y-o-y to 552,000 sq ft (NFA) by the end of 2023, indicating an improvement in the downsizing trend among corporates.

The office demand from PRC firms gradually improved. In 2023, around 22% of the total leasing volume in Central was contributed by PRC tenants, compared to only about 6% recorded in 2022.

Furthermore, 57% of new lettings and expansions in 2023 were for spaces of 10,000 sq ft or smaller, compared to 39% in 2019. This indicated that the leasing market was primarily driven by small and medium-sized occupiers this year.

Looking ahead, Sam Gourlay, Head of Office Leasing Advisory, Hong Kong Island at JLL, said: “We may see more large space transactions next year. With the completion of new and high-quality projects in 2023 and 2024, tenants in need of multiple floors will have a rare opportunity to choose from a diverse range of premium options. Anchor tenants can enjoy a rental discount compared to small-scale occupiers, along with greater flexibility than we have seen in previous cycles.” “2024 will remain a tenant market, driven by upgrading demand and focusing on new buildings that also meet sustainability demands. Despite the large amount of supply which will pose pressure on vacancy rates and rents, new high-quality buildings are expected to attract occupiers seeking quality office spaces. Overall Grade A office rents will drop 5 to 10% in 2024,” he added.

Retail Market

Total retail sales growth slowed in the second half of 2023 due to the leakage in domestic spending as the growth in outbound travel outpaced inbound visitation substantially.

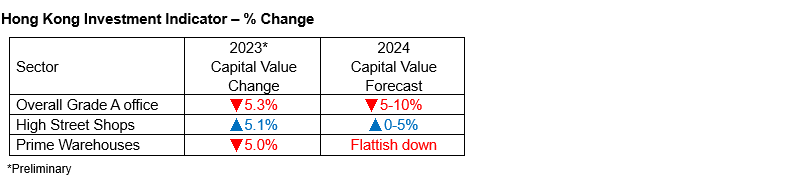

Rental values for High Street shops and Prime shopping centres rose 14.8% and 2.7%, respectively, in 2023. However, the rental growth in the second half of 2023 moderated because of domestic consumption leakage and changes in shopping patterns. High Street shops’ rental values are still over 70% below the historical peak in the third quarter of 2014. Vacancy rate in High Street shops hit the lowest since Covid-19, down to 11.6% by the year-end.

Tourism-favourable trades such as pharmacy, light refreshments and beauty and cosmetics are the most active in the leasing market in the second half of 2023. Meanwhile, retailers from overseas and mainland China continue to find Hong Kong attractive. The proportion of mainland Chinese brands making their first commerce in Hong Kong also increased from 5% last year to 24% this year, the most active among the new incoming brands. Oliver Tong, Head of Retail at JLL in Hong Kong, said: “Looking forward, the retail sector is still set to continue to recover in 2024, although there are downside risks due to domestic consumption dampened by a strong Hong Kong currency and the frequent Northbound travel by Hong Kong people. We also found that some international brands have regained confidence in Hong Kong’s retail market and are considering expanding their presence in the city after a fashion show held by an international brand. We expect the rents of High Street shops will still enjoy higher rental growth in 2024 as most prime shops having been taken up, rising 5 to 10% next year, while rents of Prime shopping centres will climb 0 to 5% only.”

Capital Market

Investors remained prudent towards commercial property investment due to high interest rates. The total investment volume of commercial properties sold for HKD 50 million or more was HKD 16.5 billion in the second half of 2023, dropping 4.7% from the first half of 2023.

But the market recorded more corporate/occupier buyers, with transaction volumes increasing by 1.05 times in the second half of 2023, compared to the first half of the year. This indicated a growing dominance of end-user buyers in the commercial property market, which is a common trend during a downturn.

The revival of inbound tourism led to cash-rich local investors targeting prime retail properties in core shopping areas, particularly Causeway Bay and Central. This drove the investment momentum of High Street Shops to pick up slightly in the second half of 2023 and the capital value of these shops rebounded by 5.1% this year, compared to a fall of 7.6% in 2022.

Eunice Tang, Executive Director of Capital Markets at JLL in Hong Kong, said: “Since the investment market will remain under the pressure of high interest rates, investors are likely to seek properties with value-added potential and explore new property sectors. In light of the talent-attracting policies and the projected increase in non-local talents and students, talent accommodation is poised to become the emerging sector in 2024. This includes the conversion of hotels into student housing and youth hostels to meet the surging demand. The most optimal hotel for student housing conversion will be those that have less than 200 room keys.” In terms of market performance, she believes retail properties will outperform the overall market, projecting their capital values to rise 0 to 5% in 2024. However, capital values of Grade A office will drop 5 to 10% and prime warehouse will be flattish down.

Residential Market

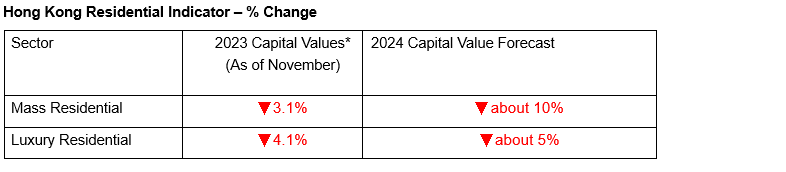

The residential market turned more sluggish in the second half of 2023 as buyers are cautious amid rising interest rates and the challenging external environment. Mass residential saw a decline of 3.1% in capital values as of November 2023, bringing them back to the price level of March 2017.

Prices of luxury residential fell 4.1% during the same period. However, luxury residential rents rebounded by 4.9%, as there were sustained demand from potential buyers switching to the leasing market and the inflow of talents and non-local families.

Total residential sales remained low, with the average monthly transaction volume in the first 10 months of the year being 25% below the previous four-year average.

Joseph Tsang, Chairman of JLL in Hong Kong, said: “The policy relaxation had no impact on the housing market. Developers started offering double-digit price discounts to clear inventory more aggressively than before. The underperformance of stock market has had a lagged effect on the housing market. Although consensus anticipates rate cuts starting in mid-2024, local banks may not immediately align due to tight liquidity and currently higher deposit rates compared to mortgage rates. Furthermore, even with potential decreases in mortgage rates next year, it is mistaken to presume that this will automatically lead to a rebound in prices. We believe the housing prices will continue to fall, with mass residential prices expected to decline by a further of about 10% in 2024, reaching levels last seen in 2016.”

Tsang believes home prices are unlikely to experience a significant rebound due to the government plans to build 39,100 subsidised sale flats in the next five years, which will dampen demand in the private housing market. Buying demand from mainland Chinese will be limited and primarily focused on the luxury market.

Without support for the downward momentum, negative equities are expected to increase to about 30,000 cases if the home prices drop a further 10% next year.

“The weakening property market will negatively impact the city’s economic growth and consumer spending. It will also depress the government’s land revenue, which is a major source of income,” Tsang added. “The government should revise the housing policies to support the residential market.”

Tsang suggested the followings:

- Remove all cooling measures.

- Provide interest-free loans to assist the young generation of first-time buyers in getting on the property ladder.

- Prioritise on public rental housing and set a clear distinction between private and public housing markets.

- Speed up infrastructure developments in existing residential clusters, especially in Kai Tak.

Land Market

As of November, only 14.2% of the current fiscal year land premium revenue target was achieved and six government land sites were withdrawn from tender. With only one quarter left in the fiscal year, it is unlikely that the land sale revenue will reach the estimated target of HKD 85 billion.

High interest rates and weak home sales are causing developers to be conservative in tender, which could lead to more withdrawals in the coming months. Such frequent withdrawal of government land tender will significantly reduce land revenue, funding for future infrastructure developments, and market sentiments.

For lease modification and land exchanges, developers are increasingly opting for the traditional land premium application scheme instead of Standard Rates. This shift is driven by the sharp fall in land prices. For example, a developer paid at least 39% less by utilising the traditional scheme for the redevelopment of a cold storage in Yau Tong into a residential project, compared to the Standard Rate.

The growing disparity between market prices and Standard Rates will diminish the effectiveness of Standard Rates in expediting the land premium procedure, further slowing down urban renewal and new area development.

Alkan Au, Senior Director of Value and Risk Advisory at JLL, said: “Therefore, it is time for the government to review land policies to alleviate the current stalemate and at least improve the probability of continuing the land sale to keep the city’s development moving.”

He suggested the following:

- Review Standard Rates more frequently, ideally every six months.

- Resume government land sales by application list to increase the likelihood of successful land sales and avoid damaging knock-on effects on the market.

- Prioritise projects with stronger interests from developers and slow down less time-pressing mega projects such as Kau Yi Chau Artificial Island, given the decline in land revenue and limited funding for future infrastructure projects.

For further information, visit jll.com.