(18 January 2024, Hong Kong) Global real estate services firm Cushman & Wakefield today published its Greater Bay Area Residential and Investment Market 2023 Review and 2024 Outlook. Although the GBA’s residential and investment markets were yet to see a significant rebound following China’s full border reopening, housing market sentiment stabilized in 2H 2023 as China’s central and local governments gradually relaxed residential market control measures.

Meanwhile, the CRE investment market (large-sized deals at >RMB 100 million) also saw mainland capital and state-owned enterprises more active in reviewing their strategies and seeking investment opportunities. Looking ahead, 2024 will be a year of recovery. The improving transportation network, and expectations of more favorable policies to be introduced to the market, will bring further support to the GBA residential and investment markets.

GBA Residential Market

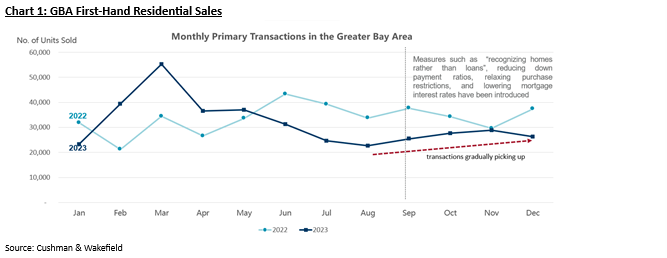

Buying sentiment in the GBA residential market remained generally cautious in 2023. However, since the central government announced plans to ease controlling measures in late August, some GBA cities have adjusted their housing policies, including “recognizing homes rather than loans,” reducing down payment ratios, relaxing purchase restrictions, and lowering mortgage interest rates, in turn helping to release pent-up demand and enhance potential buyers’ confidence in the residential market. As a result, following a decline in GBA primary residential sales since March 2023, the market bottomed out in August and gradually stabilized towards the end of the full year 2023. Total transaction volume in November 2023 was up 27% from August (Chart 1), bringing the total annual transaction volume to around 378,000 units, a 6.2% y-o-y drop from 2022.

Alva To, Cushman & Wakefield’s Vice President, Greater China & Head of Consulting, Greater China, said, “According to past experience, it usually takes some time for the market to digest and react to new policies. Therefore, although the residential transaction volume will not likely rebound significantly in the short term, it is expected that the entry barriers of potential buyers can be eased under the relaxation of regulatory measures. Policies such as ‘recognizing homes rather than loans,’ lowering down payment ratios, and relaxing purchase restrictions are helping to restore purchase demand from upgraders looking to change their homes. Looking ahead to 2024, with the deepening integration of the GBA, we expect more Hong Kong residents will consider buying housing assets in GBA cities, and the current strengthening of the HKD against the RMB is also beneficial to Hong Kong buyers entering the market. With the increasing transportation connectivity in the GBA, the residential market will likely benefit from more convenient mobility, and the government’s urban redevelopment and industrial strategies will help restore stability in the residential market. We forecast that average monthly first-hand residential sales in 2024 will reach about 33,000 units, and the total annual transaction volume is expected to increase by 5% to nearly 400,000 units.”

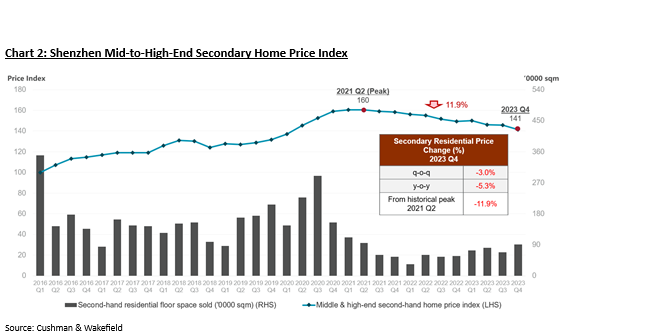

Regarding secondary market home prices, which generally better reflect current underlying trends, Cushman & Wakefield’s Shenzhen price index for mid-to-high-end secondary market housing continued to trend downwards in 2023, and the price correction in Q4 slightly expanded, bringing the full-year drop to 5.3% y-o-y compared to 2022 (Chart 2). Throughout 2023, the GBA residential market was still in a consolidation phase, where potential buyers tended to adopt a wait-and-see attitude as they were generally expecting the government to ease restrictions and introduce more policies to stimulate the housing market, in turn impacting the overall transaction volume and price levels. However, the gradual relaxation of control measures at the end of Q3 2023 is likely to help restore market confidence and drive up transaction volume, supporting residential property prices to stabilize in 1H 2024.

GBA CRE Investment Market

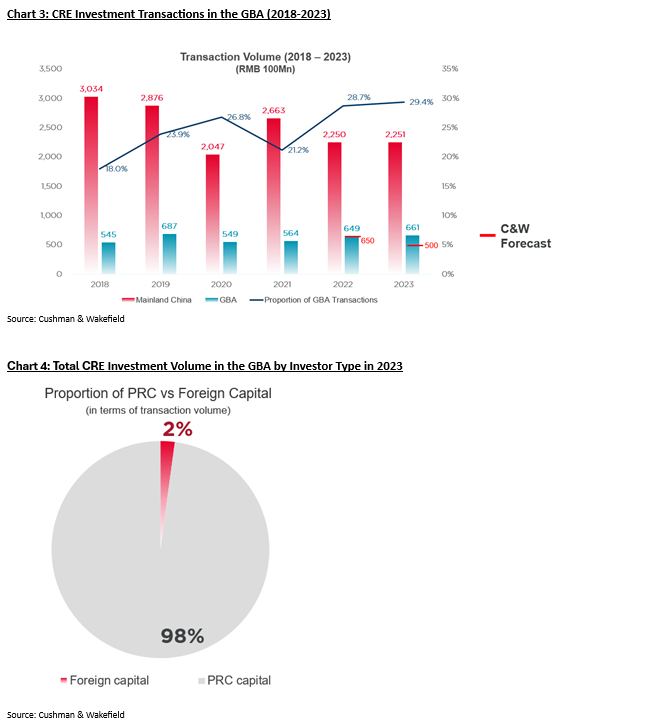

Despite the global high interest rate environment, GBA CRE investment market (large-sized deals at >RMB 100 million) performance was relatively stable in 2023, with the total annual investment volume reaching RMB66.1 billion, marking the second-highest level of the last five years. Investment volume in the GBA accounted for about 30% of the overall mainland China investment market, representing a significant jump from 18% in 2018 when the GBA initiative was first introduced (Chart 3), reflecting investors’ growing interest in GBA CRE properties. As for transaction numbers, on the back of improving buyer sentiment in the second half of last year, there were a total of 85 transactions in the GBA area in 2023, the highest in three years.

Charli Chan, Cushman & Wakefield’s Executive Director & Head of HK PRC Team, Capital Markets, commented, “The total 2023 GBA CRE investment volume was close to that of 2019, accounting for 29.4% of the overall mainland China investment market. This amount surpassed our earlier forecast from the mid-year, indicating that investors have become more active in pursuing opportunities within the GBA initiative. With offshore RMB lending rates much higher than onshore rates, overseas institutional investors have often been restructuring their asset allocation amid a high interest rate environment, hence slowing their pace in the investment market. At the same time, some real estate funds are more willing to offer discounts to attract buyers when disposing of mainland China assets. In contrast, mainland capital sources including state-owned enterprises, end-user buyers, and private investors are relatively active, seizing the opportunity to bottom-fish for long-term investment while property prices are more rational amid the relatively low borrowing rates in mainland China. In fact, domestic capital accounted for 98% of the total transaction volume in 2023 (Chart 4).”

GBA CRE Investment by Asset Type

In terms of property type, traditional office and R&D-focused office assets continued to attract investors’ attention, accounting for over half of the total investment volume in 2023. Over the past few months, investment appetite in commercial projects has gradually picked up, with cases of en-bloc transactions involving receivership deals where transacted prices were more attractive than the pre-pandemic level.

Charli Chan concluded: “Looking forward to 2024, interest rates in mainland China are likely to remain at a low level, which will help support GBA investment and financing activities. Traditional property investments are expected to focus on high-end logistics portfolios with value-added potential. Meanwhile, the C-REIT market total value has now exceeded RMB100 billion, with an increasing number of underlying asset types, where industrial parks, rental housing, and consumer-related infrastructure projects also attracting investors’ attention. In addition to seeing insurance capital and financial institutions focusing on core assets with stable returns, local corporates and state-owned enterprises are actively looking for opportunities to purchase core assets in first-tier cities. We believe that investors will have more choices and opportunities in 2024, as more quality assets in the GBA will likely offer price discounts.”