(4 October 2021, Hong Kong) The number of real estate technology startups has increased 300% over the past decade, seizing the opportunity to address the industry’s biggest challenges through technology. Data released by JLL (NYSE: JLL) suggests that opportunity continues to abound in the sector’s startup landscape, with over US$9.7 billion of funding activity in the first half of 2021, the most active first half on record. Additionally, the market shows signs of maturation as funding begins to shift toward established players and increasing consolidation drives the emergence of industry leaders.

“While real estate technology adoption was on the rise before the COVID-19 pandemic, it has become essential for today’s leading real estate players, buildings and spaces,” said Ben Breslau, Chief Research Officer at JLL. “Technology is at the center of the most important trends shaping business and real estate. That includes hybrid work, health and safety, and sustainability initiatives, all of which are in high demand. That’s why we expect funding within this sector to break records this year.”

“Our industry is right on the cusp of impactful change driven by widespread technology adoption,” said Raj Singh, Managing Partner of JLL Spark, the global venture fund of JLL Technologies. “The trends we’re seeing suggest there may be no better time to invest in real estate technology. The opportunity to shape the industry for the future by supporting innovation holds great potential for strategic change as well as return on investment.”

The evolving property technology (proptech) landscape

Amid the 4th Industrial Revolution, and accelerated by the COVID-19 pandemic, new technologies have proliferated to take advantage of developments in computing power, analysis and connectivity. The number of startups across the real estate industry has grown rapidly in the past decade—from under 2,000 to nearly 8,000—as companies look to apply these new technologies.

With that said, there has been a migration in funding and mergers and acquisitions (M&A) to more established industry leaders.

Venture capital and M&A trends

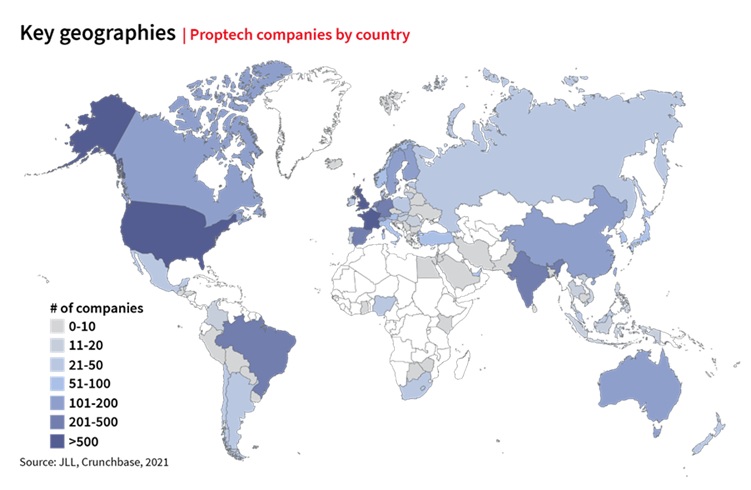

The nearly 8,000 companies, identified by JLL, that provide technology solutions in the built environment have collectively raised more than US$97 billion of equity funding in the past decade. Built environment technology startups can now be found in most countries around the world.

- In alignment with the wider tech ecosystem, the U.S. continues to account for the most company conceptions and fundraising—50% of funded companies over the past decade. U.S. cities and regions hosting the greatest number of proptech startups include New York, San Francisco, Los Angeles, the Silicon Valley and Chicago.

- Although China has significantly fewer companies, it is the second largest market in terms of funding, with more than US$16 billion raised since 2010. India, Singapore and Australia have been the principal markets for fundraising outside China in Asia Pacific. Top cities include Bengaluru, Delhi, Singapore, Beijing and Sydney.

- In Europe, the UK and Germany make up the majority of fundraising across the region, followed by France, Spain and Sweden. Top cities include London, Paris, Barcelona, Berlin and Helsinki.

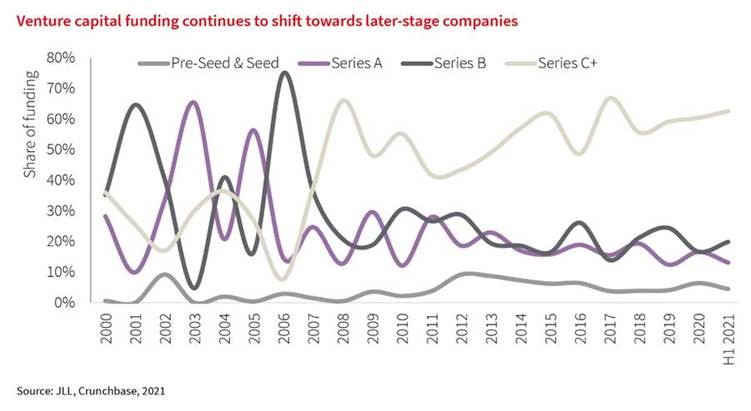

While the pandemic accelerated engagement with new technologies, it simultaneously impacted funding for early-stage companies in the real estate sector. The industry also shows signs of increasing maturation.

- According to Crunchbase, early-stage venture was down in 2020 by 11% year over year. JLL found that venture capital equity funding to built environment technology was notably impacted, slowing to US$13.4 billion in 2020, down 19% from US$16.6 billion the previous year.

- However, investment has accelerated in 2021 with H1 funding activity of US$9.7 billion, up from US$8.8 billion in H1 2020 and the most active first half on record.

- As the sector matures, funding is also migrating toward more established companies, with the majority of capital invested in later-stage funding rounds and in products with strong adoption post-COVID.

- This maturation, combined with a more difficult fundraising environment, is contributing to greater consolidation in the sector. In 2020, M&A activity was at a record high of US$21.9 billion, and it is already above US$18 billion so far in 2021.

Challenges and opportunities

COVID-19 has proven an opportunity to experiment and accelerate technology adoption across the real estate industry, with potential to make buildings more sustainable, healthier and more human-centric. A recent JLL survey found that, among nearly 650 leading global occupiers and investors, the top priorities are to create places that are human and green.

Occupiers are taking a transformative approach to carbon reduction by embedding sustainability into their business models, with 89% stating that sustainability is increasingly important to their corporate strategy. Real estate investors believe focusing on decarbonization can deliver value and a competitive advantage.

However, a range of issues are slowing progress, including a fragmented technology landscape, lack of industry standards, privacy and security needs, and more. Responding to these challenges will require greater cooperation and collaboration among technology firms, property companies and the industries they service, as well as national and urban governments. “Recent events across the globe have highlighted the importance of addressing our industry’s impact, and leaders are taking this to heart,” said Singh. “Proptech startups and more established tech and real estate firms are at the forefront of solving the industry’s challenges—with benefit to the world at large. Continued investment in these companies is an investment in the future of real estate.”